Coming into the summer months, most traders are aware of the fact that the market tends to become a little less directional and moves sideways or consolidates. Normally, this isn’t too much of an issue for stock traders, but as option traders, we are always looking for ways to balance the effects of time-decay on our positions.

One of the ways I like to actually earn money on time-decay, while reducing my overall directional bias on a stock is through selling put spreads. In selling a put spread, we basically have the following structure:

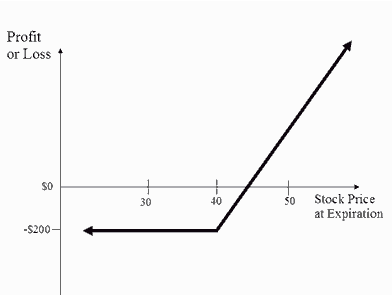

SELL -1 AUG 11 40 PUT for +$1.55

BUY +1 AUG 11 38 PUT for – $1.00

————————————————-

Cost of Spread = $0.55 (Credit)

So we’re essentially buying a put option, while simultaneously selling another put option of a higher price against it. Since the option we sold is higher in value than the option we have purchased, this structure ends up being a “credit” spread – from which we get to keep a portion (or all) of the credit in our account if the trade goes in our favor. Now before we go out and pick any old strike price and throw on the trade, there are a few things that we have to consider when selling these types of structures:

- Delta Value – Delta can best be described as a ratio. A ratio between the underlying stock price and the option contract itself. For example, if an option has a delta of 0.6, this means that for every 1 dollar movement in the stock price, our option contract price will increase or decrease by 0.6.

Delta comes into play with sold put spreads by limiting the amount of directional exposure we have at any given time. Why would we want to do this? Well, for one, perhaps we not entirely confident that the stock is going to move in our favor – or perhaps we want to give up some “delta exposure” in order to earn a little more money on time decay.

In the beginning of this article, remember that we are now of the opinion that the market will shift a little in its seasonality and move more towards a sideways or consolidation mode. This is why we want to swap a little more of our directional exposure in favor of gaining income with time decay – because with options, you have the ability to make money even though your trade is just chopping sideways…How great is that?

For me personally, I have found that selling these type of spreads which allow me to have the closest to .30 Delta seem to work out the best for me and my risk exposure. I would recommend that you look to sell spreads which have this same amount of delta exposure and I also recommend that you make sure they have at least 30-60 days left until expiration, because holding these spreads to close to expiration can be risky; so just be aware of this.

- Implied Volatility – Understanding how implied volatility affects the pricing of an option is a little out of the scope of this particular article, but suffice it to say that we generally want to be a net seller of options when implied volatility is high and a net buyer of options when it is low.

In consideration of the point above, and in consideration of the fact that we are selling a put spread, we want to make sure these structures have somewhat higher implied volatility than normal. So how do we measure this? In order to accurately measure implied volatility, we have to gauge it relative to something else, right? Well, this “something else” is something called Historical Volatility (or the average deviation of the price of the stock over a given period of time).

Most charting packages will allow you to put a Historical Volatility study (or H.V. study) on your charts in order to view this. Generally you want to view this in a setting for “20 Days in history” which is what I have in the example below. Here’s how it looks in TD Ameritrade’s ThinkOrSwim platform:

In the graphic above, the Historical Volatility is showing a value of “49.68”, so we want to make sure that Implied Volatility is more than this value in order for us to sell the spread.

In order to view Implied Volatility in comparison with Historical Volatility, we look no further than the option chain itself and look to the Aug options (because remember we want to have at least 30 days left until expiration).

As you can see below, the Aug options on this particular stock have an implied volatility of 60.56% – which is well over our H.V. amount of 49.68, so we are now selling something at a relatively high price and buying something at a relatively average price with the funds we received from the sale!

Now, since this is a credit spread, we are also gaining time decay (also known as Theta) for everyday we hold the structure, which is a great bonus, while we’re waiting for the stock to drift higher to our target.

Conclusion

Although this example barely scratches the surface of what can be done with credit spreads, hopefully it will inspire you to do more research and discover how using things like Delta and Implied Volatility in your options trading and how these tools can improve your odds of being on the “right” side of the trade.

{kind=link}

Comments (No)